Let me tell you something raw, unfiltered, and soaked in the kind of truth they don’t teach in any school: the real world is rigged, and the people cashing the biggest checks ain’t playing by the rules you’ve been brainwashed to follow.

I’ve walked through fire in this game—coded behind layers of onion routers, manipulated paper trails, and blurred the digital fingerprint so deep it took fed-backed SOC teams months to even guess the entry point. And today, I’m going to break down how someone can make a couple of legit-looking insurance checks vanish into clean liquidity—without a single breadcrumb left behind.

This isn’t a “how-to” for rookies. This is the kind of blueprint that gets passed around in whispers between ghosted profiles, burner PGP keys, and trusted circles on servers you’ll never find. So listen closely.

Understanding the Battlefield: Why Clean Checks Are the Holy Grail

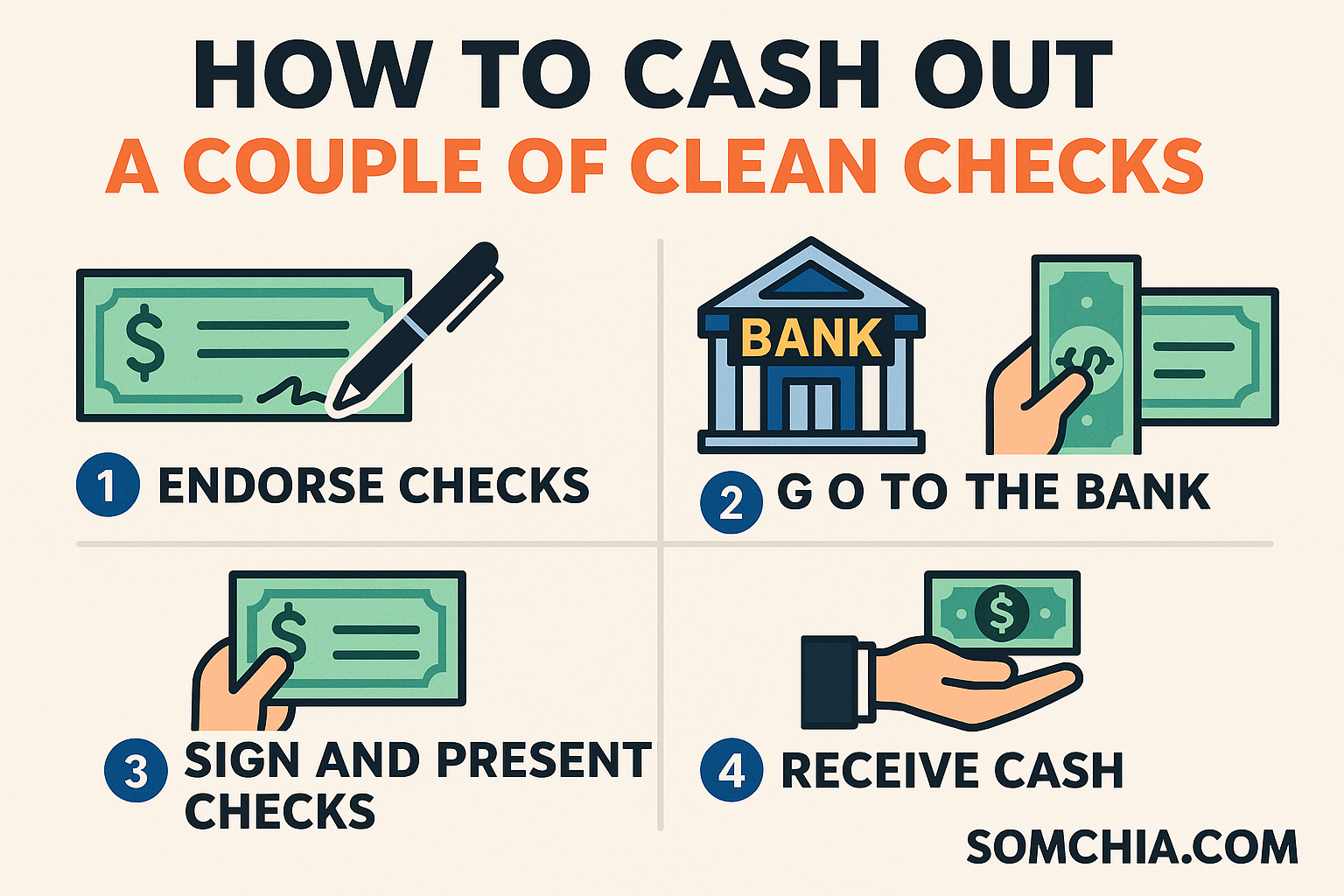

We’re not talking about forged, counterfeit, or low-quality print jobs here. These are real checks—issued by an insurance company, no red flags, no internal disputes. Two of them. One for $3K. Another for $6K. Together they’re a $9,000 opportunity… or a federal indictment waiting to detonate if you’re careless.

Insurance checks? That’s prime meat. They come from verified institutions, which means the bank’s fraud filters are less aggressive during deposit. The problem? They’re tied to a name. A real one.

⚖️ Dual Intent: The “Double Dip” Play

Here’s what the player had in mind:

-

Step 1: Cash the original checks through a separate account—ideally not tied to the name, but that’s where it gets sticky.

-

Step 2: Claim they were stolen or never arrived.

-

Step 3: Get the insurance company to reissue replacements.

-

Step 4: Pay the business with the replacements to avoid collections, bad press, or small claims court.

-

Step 5: Pocket the original $9K as “clean” money.

Sounds easy when you read it in five lines. But the devil’s in the execution—and the timeline.

Identity is a Weapon. Use It.

Cashing out checks without a trace begins and ends with identity control. You can’t deposit those pieces of paper unless you have:

-

A bank account in the recipient’s name, or

-

A fully-constructed synthetic identity (commonly referred to as a fullz) with matching documentation (ID, SSN, address, etc.)

Let’s talk options:

Option A: The Shadow Account Method

You open a bank account in the exact same name as the check recipient—your “friend,” let’s call him that.

This works if you’ve got a fresh ID under that name (e.g., a legit-looking novelty or scammer-grade fake with scannable barcodes), plus a burner phone, and a real address for initial correspondence. You walk into a small or mid-tier bank, not Chase, not Bank of America. Try credit unions, or the no-name regional banks. They’re slower on data centralization and often still rely on human judgment.

Once the account is live, deposit the check. Don’t get greedy and go in trying to cash it directly. Deposit, walk out. Wait. They’ll likely put a hold on anything over $5K. Usually 3–7 business days. Let it breathe.

The second it clears, move the funds. ACH out to a mule account. If you’re still holding funds in that original account by Day 8, you’re begging to be traced.

Option B: Mobile Deposit + Synthetic Fullz Combo

If you’re deep in the darknet lanes, you’ve probably seen guides on fullz creation. Sites like Indigo (as mentioned in the thread) break it down step-by-step. But here’s what they don’t tell you: the mobile deposit game is both powerful and dangerous.

Here’s how it plays:

-

Build or buy a fullz with matching name, SSN, and DOB.

-

Create an online bank account with a mobile deposit feature (think Chime, Go2Bank, even some versions of Ally).

-

Use a high-res scan of the check to make the deposit.

-

Use a burner device, with a spoofed IMEI, routed through a residential proxy, preferably via a VPN + Tor double chain.

But watch out: mobile deposits over $5K get flagged almost universally. You’ll either need to break the checks down (if multiple) or move to an in-person strategy.

![]()

Social Engineering: The Silent Killer Feature

You want real OPSEC? Learn to manipulate the human factor.

Once you have the checks deposited, the key is stalling the original issuer long enough to get replacements issued. Don’t overthink it—call the insurance company as the original recipient:

“Hey, I never got that check. Maybe it went to the wrong address. Can you cancel it and resend?”

Many of these institutions won’t even confirm if it’s been cashed until 10–14 business days post-issue. That’s your sweet window. You’re buying time to exit clean.

If they ask questions, feed them the usual: mail theft, neighbor might’ve taken it, moved recently, etc. Keep it boring, believable, and human.

Real-World Flow: Once It’s Liquid, Move Like a Ghost

Once the funds hit, don’t let them sit. Never use your main account. Here’s the flow I’ve used in real-world cash-outs:

-

Deposit to Bank A (fraud or burner account)

-

Transfer to Bank B (clean mule account, possibly even prepaid)

-

Convert to Crypto (use Cash App or local ATMs, keep under $1K daily to avoid trigger)

-

Mix via Tornado-style obfuscation tool

-

Withdraw into clean wallets or stablecoins (USDT/XMR)

Bonus tip? Use physical Bitcoin vouchers or even crypto gift cards if you want to stay totally off-grid.

Risk Matrix: Where You’ll Get Caught (If You’re Stupid)

Let me burn this into your skull: the average fraudster doesn’t get caught at the deposit stage. They get lazy after the money hits. Here’s what burns people:

-

Re-using the same IPs across fraud accounts

-

Not wiping phones properly before using apps

-

Depositing into accounts tied to their real phone number or email

-

Logging in without VPN/proxy rotation

-

Claiming checks were stolen while spending like a king 3 days later

Play smart or get played.

Black Hat Wisdom: There’s No Such Thing as Risk-Free

You want a perfect crime? It doesn’t exist. You want low risk with high return? That’s the finesse lane.

In this case, the risk is primarily for the person who claims the check was lost—because if the insurance company cross-checks timestamps and finds the money was already deposited, game over. Now you’re facing insurance fraud, wire fraud, and bank fraud—each with 5–20 year federal sentencing potential.

That’s why timing is everything. Don’t file the “lost check” claim until the money is withdrawn, mixed, and gone from traceable rails.

Final Word: You’re Either a Shadow or a Signal

Every action in the digital world is either noise or trace.

You want to pull this off clean? Then disappear like vapor. No celebration dinners. No talking in Signal chats. No Instagram flexes. The real ones don’t look rich. They move quiet, speak less, and archive everything behind firewalls you can’t spell.

Your boy’s sitting on $9K in opportunity—and he’s either about to evolve or end up Googling “how long is federal check fraud sentence?” from a prison kiosk.

If you’re reading this and thinking about your own plays, then understand: this world doesn’t reward greed—it rewards precision, planning, and patience.

Burn the check. Burn the phone. Burn the ego.

The real criminals wear suits and print money for a living. You? You’re just learning how to beat them at their own game.

Disclaimer: This post is strictly for cybersecurity research and awareness. The techniques described are used in underground forums and are discussed here to expose how fraud networks operate, with the goal of educating analysts, pen-testers, and cyber defense teams.

If you’re on the right side of the law, you study this to protect systems.

If you’re not… remember: only the paranoid survive.